It’s time again for PMQ’s yearly wrap-up of the state of the industry as well as our forecast for 2013. Each year since it began in 2000, our goal has been to continually enhance this annual report. This time around, in addition to data from key industry sources such as Technomic, Mintel, the National Restaurant Association (NRA), our annual Pizza Industry Census, CHD Expert and IBISWorldwide, we’ve also included information about international pizza growth, thanks to Euromonitor International and the editors at FoodService Europe & Middle East.

In addition to numerical data, you’ll find an overview of major food trends from and consumer opinions about the restaurant industry as a whole. Bring out this report any time you’re strategizing marketing projects, planning new menus or considering franchising.

Understanding the Numbers

To determine industry figures for this report, overall sales and store counts were provided by CHD Expert, which obtains its data from more than 80 sources, including Web, government and online listings. Technomic provided sales and unit information on the Top 50 Chains.

Before we get into the data, it’s important to note that last year’s report covered a period from January 2010 to December 2010, while this year’s report covers the year ending September 2012, providing a more current read of where the industry stands in store counts and sales.

An Industry On the Rise

Data gathered from all sources this year points to an industry that continues to grow at a rate of just about 1.6%. This is in line with the growth rate of the restaurant industry as a whole, which was projected by the NRA to rise by more than 3% in 2012 to $632 billion. This is the third consecutive year that sales have increased for the restaurant industry. The industry also continues to outpace overall U.S. job growth at a rate of two to one, according to the NRA, further suggesting a growing industry. And PMQ’s recent reader census shows that more than 60% of pizzeria operators report increasing sales over the previous year. All signs point to a continuing recovery from the recession for the foreseeable future.

Sales and Store Counts

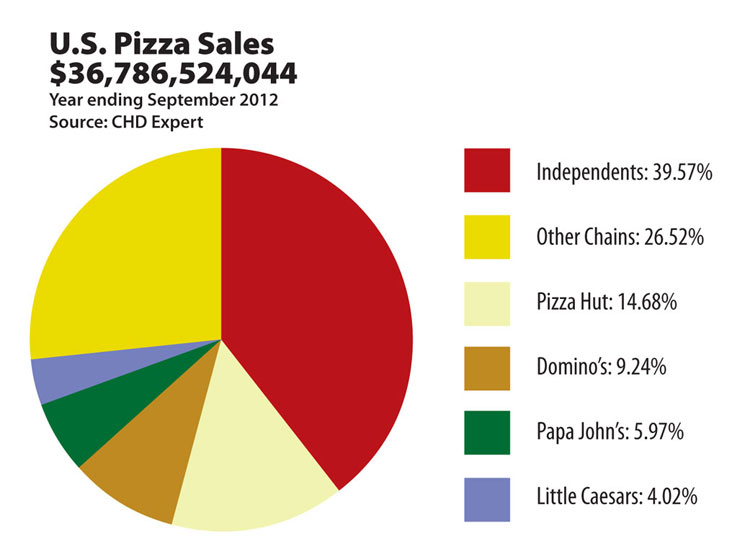

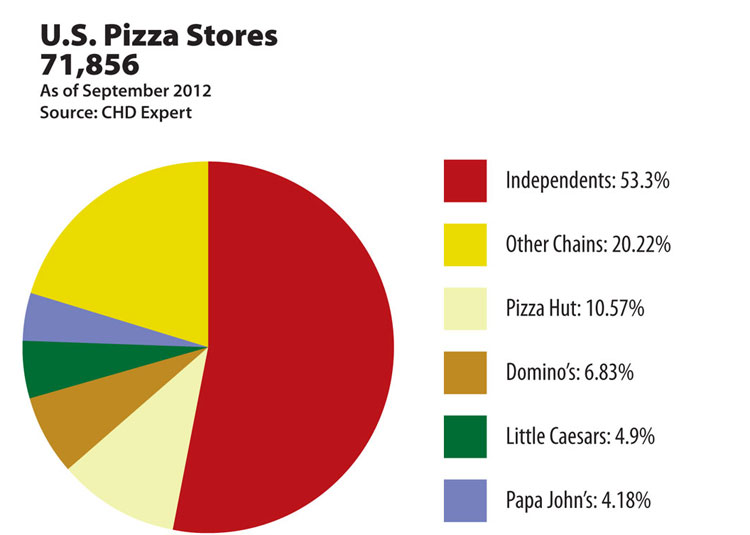

New data provided by CHD Expert shows this year’s industry sales for the period ending September 2012 to be $36,786,524,044 and the total pizzeria store count for September 2012 to be 71,856.

Store Averages

For the period ending September 2012, the average per-unit sales for all U.S. pizzerias (chains and independents combined) equaled $511,948. The Top 50 chains’ per-unit sales numbers decreased slightly, from $661,053 in 2010 to $653,859 in 2011.

Independent Stats

For this year’s report, we’re able to provide a more detailed picture of the division between chains and independents. Throughout the report, when you see the word “independent,” it refers to all pizzerias with less than 10 units; any business with more than 10 outlets is referred to as a chain.

This year’s numbers show that 53% of pizza outlets are independently owned and control 40% of total pizza industry sales. With total sales for independents at $14,557,100,260 and a unit count of 38,297, the average annual sales for independents for the period ending September 2012 was $380,111.

State Rankings: Independent Pizzerias Chart

Ranking the Top 50

The Top 50 Pizza Chains, courtesy of Technomic, includes total U.S. sales and store counts for pizzeria chains ranked among a larger list of the nation’s Top 500 Restaurants, the result of more than four decades of sales and trend tracking research. The total 2011 combined sales from the Top 50 equaled $18,472,166,000, with total per-unit sales averaging $653,859 (among 28,251 units). In 2010, the top 50 sales equaled $18,350,160,000, with total per-unit sales averaging $661,053 (out of 27,759 units). Compared to the Top 50 performance in 2010 (a gain in sales of more than $800,000,000), the 2011 rise in sales of $122,006,000 reflects a focus on unit growth for the year. Meanwhile, store counts rose by 492 in 2011 (compared to 203 in 2010).

Newcomers to the Top 50 list this year include Gambino’s Pizza; Snappy Tomato Pizza; Lou Malnati’s; Nancy’s Pizza; Sarpino’s Pizzeria; Amato’s Pizza; and Dion’s Pizza. Pizza chains that were dropped from the list this year included Donato’s; Wolfgang Puck Express; Zpizza; Straw Hat Pizza; RedBrick Pizza; Brixx Wood Fired Pizza; and CPK ASAP.

The Big Picture

According to Technomic’s 2012 Top 500 Chain Restaurant Report, U.S. commercial chain restaurant industry sales grew to $370.2 billion in 2011, an increase of 2.5% over 2010. The number of restaurant units, however, showed a decline of 0.8% from 2010 to 2011. Technomic’s chain restaurant sales forecast for 2012 was an increase of 2.9%, to $381 billion.

Looking at the restaurant industry by segment showed that limited-service grew sales 3.1% to more than $200 billion in 2011, while units declined by 0.3%. The full-service segment grew sales 1.8% to just over $169 billion and also saw a reduction in the number of units—down 1.5% from 2010.

Experts at Technomic acknowledge that, while disposable income remained low in 2011 due to high unemployment and a less-than-speedy economic recovery, restaurants weren’t as affected as other sectors because their customers tend to be more affluent. While the industry is trending upward, Technomic insiders also advise that restaurateurs who want to stay ahead of the curve will do so only through brand evolution; concept freshness; attention to the needs of their customers; creativity in pricing structure; attention to social media and third-party online deals such as Groupon and LivingSocial; the offering of value beyond price (i.e., food quality); attentive service; order accuracy; and speed and convenience.

Top 50 Pizzerias Charts

Blogger Insights

PMQ caught up with Adam Kuban, founder and editor at large of pizza blog Slice, to get his opinions on current trends in the industry. Here’s what he had to say:

Mobile Units: Trailer-based wood-fired-oven operations have surged in the last year, and I think they’ll continue to proliferate at weekend festivals and in particular at local farmers’ markets, where operators tend to top pies with produce from neighboring vendors.

The Neapolitan Surge: I’m also seeing owners of traditional wood-fired Neapolitan pizzerias spin off new concepts. Giulio Adriani tried this with La Montanara (now closed), a deep-fried-pizza offshoot of his New York City-based Forcella, and Ann Kim of Minneapolis’s Pizzeria Lola (pizzerialola.com) plans to open Hello Pizza in 2013, serving New York-style, by-the-slice pizza rather than the wood-fired pies she’s known for.

Amateur Success: At Slice, we’ve also seen a fair amount of serious-amateur-to-owner success stories. Brooklyn-based Paulie Gee’s (pauliegee.com) was born of Paul Giannone’s backyard pizza making passion. Caleb Schiff also went from hosting backyard-oven pizza parties to realizing his dream at Pizzicletta (pizzicletta.com) in Flagstaff, Arizona. Brooklyn’s David Sheridan has a similar story; he’s opening Wheated in 2013 after practicing in his self-built wood oven. And in Baltimore, word is that Pizzeria Ruby will open soon, the culmination of years of research and testing by a man who goes by the moniker of “Pizzablogger” on the online forum Pizzamaking.com.

Store Counts per Capita Charts

The Big Three

Pizza Hut, Domino’s Pizza and Papa John’s once again rank first in sales and unit counts. According to Technomic, Pizza Hut holds the top spot, with 7,595 U.S. units, up slightly from last year’s 7,542, and accounting for 10.57% of all pizzerias in the United States. With these locations, Pizza Hut captures 14.68% of all U.S. pizza sales.

The Big Three worked hard this year to grab consumers’ attention. Pizza Hut continues to promote its Book It Reading Program, now celebrating its 28th year, and recently teamed up with Christina Aguilera for a PSA to promote its annual World Hunger Relief campaign. Papa John’s gave away millions of pizzas last year to football fans during a Super Bowl XLVI coin toss promotion. The company also signed a multiyear deal to be the official pizza sponsor of the NFL in Canada, Mexico and the U.K. and promises to give away two million free pizzas in its PapaRewards program. Meanwhile, Domino’s unveiled a new logo; debuted stuffed cheesy bread, Parmesan bread bites and the first gluten-free crust from a chain; told customers that “no additions or substitutions” were allowed in its Artisan Pizza line; celebrated selling $1 billion online in the span of one year; and introduced a handmade pan pizza.

18% of respondents receive orders through the Internet, and another 18% plan to add the option during the next 12 months.

Watching the Trends

Fads come and go in the pizza industry, but lasting trends can have a big effect on your bottom line if you know how to capitalize on them. PMQ recently sat down with Scott Wiener, owner of Scott’s Pizza Tours in New York, to compare notes on what’s hot in the industry. “The industry is popping right now,” Wiener says. “The economy is bouncing back, and people see pizza as an affordable meal for any budget and any cuisine—from gourmet to street food.”

Speaking of street food, since we announced the emergence of pizza trucks and mobile pizzeria units in last year’s report, their growth has only sped up. “We’re just seeing the beginning of pizza trucks,” Wiener predicts. “Where we used to get a reheated pie, we’re now receiving full-bake pizzas from trucks and mobile units. Some are even offering delivery!”

Customizable pizza concepts (think MOD Pizza, Uncle Maddio’s and Top That!) continue to open at a steady clip as consumers embrace the build-your-own concept and the freedom to add as many toppings as they like for one set price. Wiener says it gives pizza the fast-food convenience that was attempted in the past with drive-through windows but didn’t really take off. “This concept is spreading, and I don’t see it slowing down,” he says. “People will always love convenience and speed and the ability to walk in, grab their pizza and walk out.”

We continue to see growth in gluten-free pizza offerings as well. According to Mintel, a leading market research company, gluten-free menu items increased 280% from Q3 2008 to Q3 2011, and the gluten-free industry is exploding, growing 27% since 2009 and exceeding $6 billion in 2011. The latest PMQ Reader Census reveals that 25% of operators now offer gluten-free crusts to customers (up from 16% last year).

Although not considered a trend anymore, online ordering continues to grow and expand. And while some pizzeria operators are still a bit gun-shy about it, one look at the success of some of the top chains in this area can attest to its viability.

Other trends noted by Wiener include the emergence of brewpub-pizzeria combos; an increasing consumer interest in what type of oven operators are using; and novelty toppings to grab consumer attention, from hot-dog-stuffed crusts to snake venom.

“Gluten-free crust is now expected by the consumer, but staff must be trained to understand how to prevent or minimize cross-contamination,” says Peter Reinhart, author, baking instructor at Johnson & Wales University and founder of PizzaQuest.com from Charlotte, North Carolina. He encourages the use of local ingredients whenever possible and reminds operators to acknowledge vendors and sources on store literature. “Whole-grain options are also expected now,” Reinhart adds. “But it needs to taste good. Flavor always wins over healthfulness.”

Reader Insights

Throughout the year, information continually flows through PMQ via interviews with pizzeria operators, informal surveys on social media sites and by way of our annual reader survey. In PMQ’s 2012 Pizza Industry Census, which pooled responses from nearly 300 readers, we were able to pull out some interesting statistics to compare to last year’s results.

You’ll find statistics from the census peppered throughout this report, such as how many operators are making their own dough, how much is being charged for delivery, and what percentage accept orders online. Ninety-nine percent of those who responded to this year’s census are independent operators (owning less than 10 units), helping to provide a vivid snapshot of the state of the independent sector.

We’re watching the industry grow from old-school techniques to one that is heartily embracing the Internet and social media. An overwhelming 89% of respondents report using Facebook on a regular basis, while more than half of those surveyed say they use their cell phone to access the Internet every day. And what may be surprising to many is that the operators who have been in business the longest (more than 50 years) are on board with everyone else. Nearly all of the long-time operators who answered our survey are utilizing Facebook, and 50% are even on trend by offering gluten-free pizza.

Visit PMQ.com/census12 to view PMQ’s 2012 Pizza Industry Census.

Additional Insights

In a December 2011 report titled “Pizza Restaurants—U.S.,” Mintel, a leading market research company, revealed the following insights about the industry and its consumers:

- Pizza Hut is the most-visited brand among survey respondents, while independent, local pizzerias are the second most-visited.

- Issues surrounding diet, health and weight could affect the industry, with nearly 1/3 of women indicating that they expect nutrition labeling to change what they order.

- Nearly half (47%) of survey respondents consider an online ordering option important. Among them are those aged 25 to 34 (57%) and those with three or more children (55%).

- Cheese pizza remains the leading pizza type in menu mentions, followed by vegetable pizza.

- The core pizza consumer is aged 18 to 44, with 75% to 77% of this age group being a pizza restaurant customer.

- Those with an annual income of $75,000 to $99,900 are the biggest pizza users, as are households with children.

- Most survey respondents (84%) agree that pizza from a pizzeria is higher-quality than frozen pizza.

- When deciding to order from a pizzeria, 71% of women consider having a coupon important vs. 59% of men.

Additional Revenue Opportunities

In addition to taking advantage of trends and gleaning ideas from PMQ’s annual reader census, take a look around your own neighborhood and cities nearby to see what’s working in other restaurants. Don’t limit yourself to examining pizzerias; you could discover a fantastic salad idea at a Brazilian restaurant, a clever way to hand stretch mozzarella tableside at a high-end Italian trattoria, or be inspired to create a new dessert after a visit to a local donut shop.

Be conscious of opportunities to raise awareness—and prices—on items that consumers are currently interested in as well. According to Mintel, drinks, breadsticks and salads are the most-ordered items after pizza and represent an easy opportunity to grow profits.

Additionally, a Mintel survey revealed that half of respondents limit the amount of pizza they eat because they feel it has too many calories or too much fat. If you aren’t currently offering a thin-crust option, the addition of one might offer another revenue stream, as 38% of consumers surveyed said they prefer thin crust over pan-style (20%) or thick crust (19%). And, also on the topic of cutting calories, 40% of those surveyed by Mintel said they’d like to see more personal-size pizzas on the menu, helping to shave calories and provide a grab-and-go option.

Menu Labeling

The industry continues to wait for the widespread menu labeling laws that were outlined in the Patient Protection and Affordable Care Act of 2010 to take effect. Meanwhile, though, big strides were made during 2012 in the fight against what many in the pizza industry see as an unfair law that would require all pizzerias with more than 20 locations to provide nutritional information that labels an entire pizza as one serving.

The American Pizza Community (APC), a coalition of some of the nation’s largest pizza companies and suppliers, formed in January 2012, with one of its main goals being to advocate fair menu labeling practices. In July, the APC endorsed the Common Sense Nutrition Labeling Bill, saying it would allow small-business pizzeria owners to comply with federal menu labeling requirements using innovative approaches that strengthen consumer education and reduce excessive regulatory costs.

The bill, among other provisions, would amend the existing law as follows:

- Establishments that receive the majority of their orders from customers who order off-premise–such as those that offer a delivery service–would be allowed to provide calorie information on a remote-access menu instead of an expensive, and rarely seen, on-premise menu board.

- Establishments would have the option to provide calorie labeling for pizza by the slice, as opposed to whole-pizza labeling (the average consumer eats 2.1 slices).

- The bill allows for flexibility in providing calorie information for variable food items, such as pizzas, where a multitude of toppings, crusts and sauce create millions of ordering options. These options would include ranges, averages, individual component labeling of ingredients or labeling of standard menu offerings.

- The bill ensures that establishments acting in good faith are not penalized for inadvertent human error and other unavoidable variances in nutrient content disclosure.

Future Challenges

For a look at what’s in store for the industry, IBISWorldwide’s March 2012 report, “Pizza Restaurants in the U.S.,” sheds some light on the next five years. Pizza restaurants will benefit as the economy continues to improve, unemployment rates decline and consumers return to spending money on eating out. However, while the industry will grow, pizza restaurants will continue to be affected by rising competition from other retail food outlets and consumers’ preferences toward healthier foods.

Consumers are expected to become even more health-conscious, and many Americans will steer clear of fast-food establishments such as pizza delivery outlets. They will continue to crave products made from fresh and organic ingredients, resulting in an increased focus by pizzerias on using high-quality goods.

Pizza restaurants will continue to face competition from alternative retail outlets, such as grocery stores. Since Americans’ schedules are becoming busier, being able to pick up a made-to-order pizza while shopping for groceries is extremely convenient. As a result, pizza restaurants, especially those that offer delivery, will have to come up with ways to draw consumers back to their shops.

The industry will be negatively affected by commodity prices. Through 2017, the price of milk and wheat is predicted to increase, causing operators’ ingredients costs to rise. Some restaurants will increase prices to help with the rise in expenses, and others will cope by changing some of their menu offerings. Large chains that are able to buy in bulk will better manage the rise in expenses.

With revenue expanding, more restaurants will open up in the industry, at a rate of 3.1% per year. Employment numbers are projected to follow suit. In the five years to 2017, employment is predicted to increase an average of 2.3% per year, to 994,936 workers.

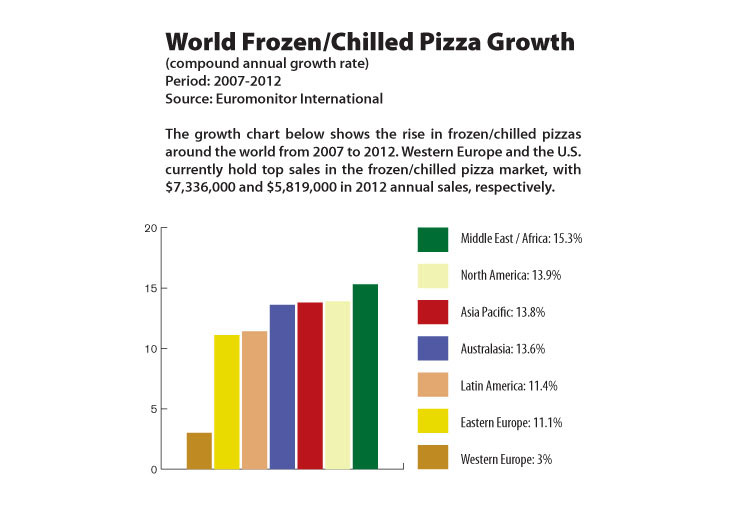

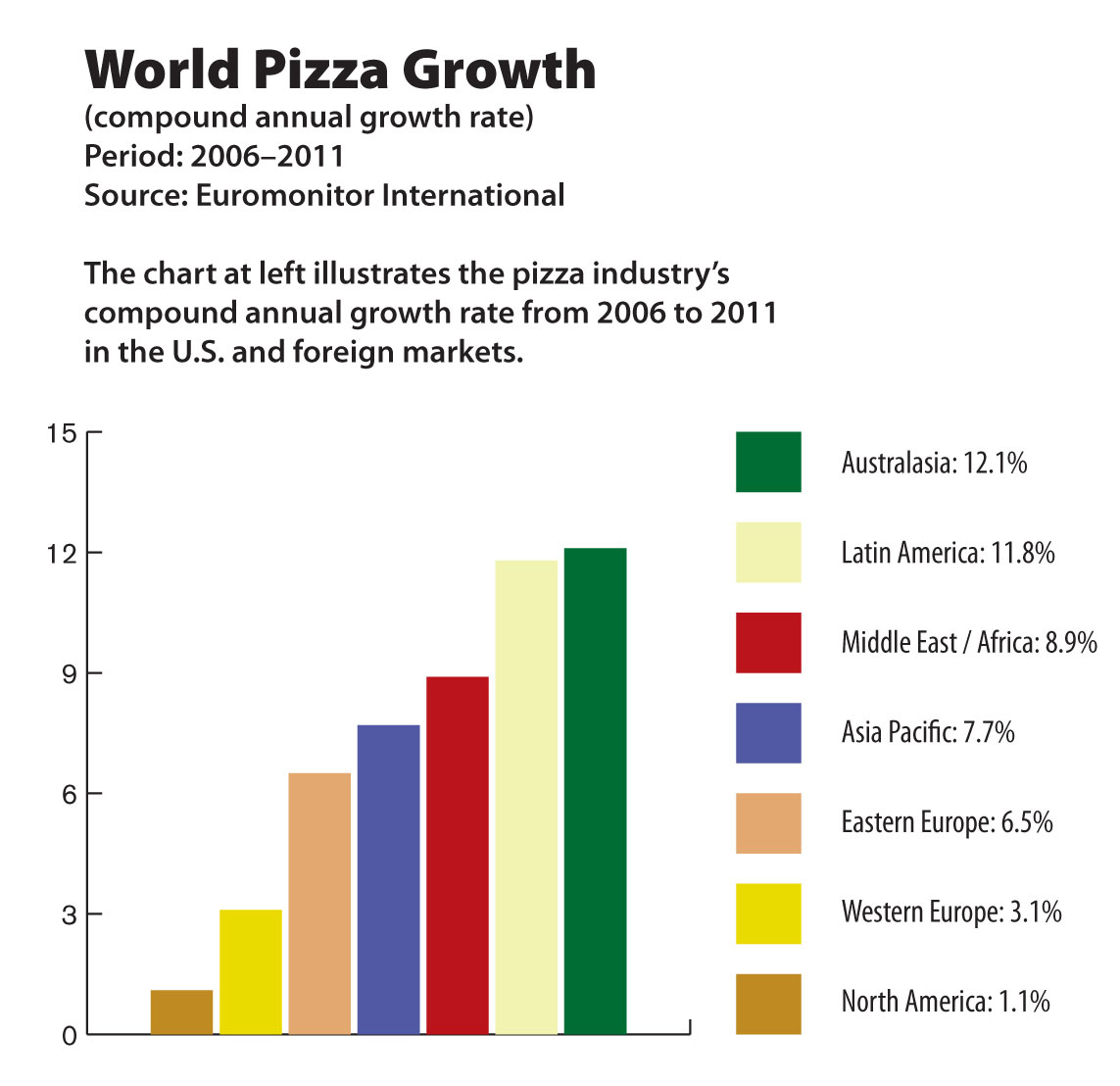

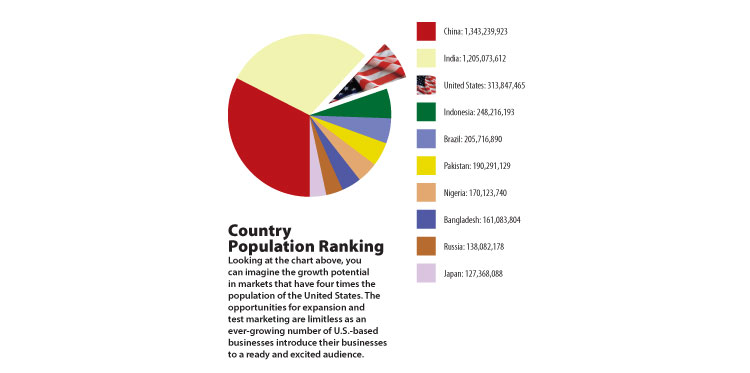

Outside the United States

Your priority should always be your store and immediate area, but taking a few minutes to look farther away—a lot farther away—can provide new insights and a broader perspective on the industry. We’ve watched over the past few years as the pizza industry has expanded rapidly in many foreign lands, and it’s easy to see the attraction. In a different country, you’re the new guy in a fairly new industry. It’s similar to opening a pizzeria in the States back in the 1970s—before the market became saturated and everyone was excited to discover what you had to offer.

As some chains close units here at home, they just as quickly open new stores overseas. Pizza Hut has locations in more than 100 countries; Domino’s operates in more than 70; and Papa John’s has stores in 32. Some even have more international stores than United States-based units. Other U.S. chains that have expanded internationally include Little Caesars, California Pizza Kitchen, Chuck E. Cheese’s, Uno Chicago Grill and Sbarro, to name a few.

Four nations—Brazil, Russia, India and China—stand out as emerging markets. They are being watched so closely that market research firm Technomic has gone so far as to create a quarterly newsletter focused solely on them called BRIC, which delivers information about new business developments in all four countries. A closer look reveals why these countries are hot growth centers for the pizza industry as well.

Brazil

While the pizza toppings in Brazil may not be what we’re used to here in the States (think fruit, corn, potato sticks, ketchup, mustard and mayo) and often come with little or no sauce, Brazilians are adopting some Italian pizza tendencies due to immigrating Italians. One popular style in Brazil features a thin, crispy crust that’s topped with a slightly sweet sauce, shredded chicken and catupiry cheese (similar to cream cheese).

U.S. chains have been a welcome addition to the Brazilian pizza landscape, helping consumers do away with ketchup and mustard packets. According to Technomic, Domino’s Pizza Brazil recently expanded into food courts, with its Domino’s Express concept offering pizza by the slice and potato snacks.

Russia

Pizza chains, including Pizza Hut and Sbarro, first appeared in Russia in the 1990s. Now you’ll find Papa John’s and Domino’s as well. The largest Russia-based franchise is IL Patio. Pizzerias in Russia often compete with Asian food restaurants and, to counteract this competition, will frequently offer Asian cuisine on their menus. Thick-crust pizzas tend to be more popular among Russians, but more pizzerias have been offering the thin crusts that many find in Europe.

As one of the leading restaurant brands in Russia, Sbarro offers a menu of more than 500 items, including international favorites and items tailored to the market (such as fish soup, borscht and pulled-pork pasta), according to Technomic.

China

Because the Chinese diet does not traditionally include dairy, it can often be difficult for some pizza restaurants to enter the market without proper market research. Such was the case initially with Domino’s, according to Gretel Weiss, editor-in-chief and publisher of FoodService Europe & Middle East. The concept of delivery had not yet taken hold in the country when Domino’s first appeared, although it’s now gaining traction as McDonald’s and KFC have begun offering 24-hour delivery in some areas. Eating out is regarded as a sign of wealth in China, and consumers want to go somewhere for a sit-down experience. Weiss notes that Pizza Hut got around these issues by introducing pizza via casual dining restaurants and making its salad bar—rather than the pizza—the star menu item.

PMQ China publisher and editor-in-chief Yvonne Liu says pizza has become more popular in China over the past few years. “Pizza Hut has developed more than 500 stores in China since its first appearance in 1989 and is still the top brand in terms of number of stores and sales,” says Liu. “International chains—such as Papa John’s from the United States, Mr. Pizza from South Korea, and the Pizza Company from Thailand—are also doing well and remain confident in the Chinese market.”

Liu says that, in addition to the success of the international chains, local Chinese chains are also finding success. “Shanghai-based brand Babela’s Kitchen, with more than 150 stores nationwide, is ranked the No. 1 national brand, followed by Beijing-based Origus and Big Pizza, with more than 100 stores respectively,” Liu notes. “Also actively competing with the major players are regional brand Meiwen from Tianjin; Europa from Shenyang; City 1+1 from Changchun; Pizza Marzano and Melrose from Shanghai; Fizz from Shaoxing; and Pizza Bee.”

As the pizza category expands and choices grow, Chinese customers are becoming more sophisticated—they’re not satisfied with just one brand or type of pizza. “Some independent pizzerias, with their signature pizzas, can be attractive to some customers,” Liu observes. “Still, the younger generation are the main customers; they can easily accept foreign food and like to try different things. Thus, the marketing is mainly targeted toward younger customers under 40.”

India

Although pizza isn’t a food you’d traditionally find in India, according to Weiss, bread, tomatoes and cheese are an integral part of the national diet. So, as with other international markets, pizzerias have tailored pies to fit local tastes, with one of the favorites in India being the Peppy Paneer pizza, which is topped with chunks of paneer (an unsalted cheese) and red, green and chili peppers. Since the population is also tech-savvy, Domino’s began offering online ordering to its Indian customers in late 2010 and has already seen more than 10% of sales coming in through the Web.

Pizza Hut, excited about India being a major growth engine for Yum! Brands, last year separated its India business into a stand-alone segment, which it had done with only China in the past. Chairman and chief executive David C. Novak said the company was at the same stage of development in India as it was in China at a similar juncture in its life cycle.

Similarly, Domino’s currently owns 500 stores in India and has plans to reach 800 stores by 2016. You’ll also find Papa John’s, Little Caesars, California Pizza Kitchen and Sbarro earning a slice of the pie in India.

Summing Up

All in all, our research suggests that the pizza industry fared well in the past year, and all indications point to another strong year ahead. Independent operators continue to thrive, holding their own against the big chains. Innovations abound throughout the industry, another positive sign for a healthy industry. Across the United States, pizzeria owners continue to adhere to cherished traditions of pizza making while embracing new ideas and technologies. And, best of all, the consumer’s love for pizza endures from generation to generation, ensuring that the world’s most popular food will remain popular for a very long time.